Unpacking the Rising Cost of Insulin and What it Means for Patients

By Ilana Orloff and the diaTribe team

Twitter Summary: We investigate the rising cost of insulin, why this might be occurring, how it impacts patients, and financial resources to help.

Bloomberg recently published an article titled “Hot Drugs Show Sharp Price Hikes in Shadow Market,” discussing the rapid rise in wholesale prices for certain prescription drugs. The article highlighted price increases for diabetes drugs and insulin in particular, noting that diabetes drugs accounted for five of the 27 branded drugs with price increases of at least 20% over the past year. Below, we investigate this phenomenon, why it might be occurring, and what people may not immediately see about dynamics in the field. Importantly, we also discuss what this means for patients and provide some resources to help patients access top branded drugs.

Table of Contents

So what is happening to insulin prices?

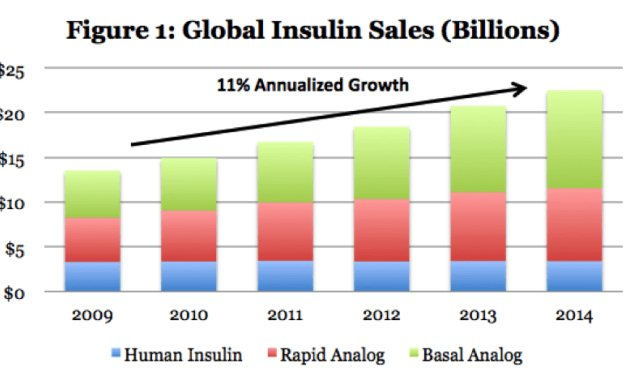

The Bloomberg article focuses on the rise in wholesale insulin prices, which approximate the price that would be displayed on a store shelf (most individuals with health insurance pay a lower, subsidized price). Several brands of insulin have seen wholesale price increases of more than 160% over the last five years, including Eli Lilly’s Humulin R (human insulin), Novo Nordisk’s Levemir (basal insulin determir), and Sanofi’s Lantus (basal insulin glargine). Lantus and Levemir prices increased by ~30% in 2014 last year. Putting this into context, the Express Scripts Prescription Price Index illustrates that branded drug prices have increased at 12% per year over the last five years while these insulin brands rose 15%+ per year (generic drug prices are down 50% on average over this period and are quite inexpensive compared to development costs).

However, this does not factor in what it means if you have health insurance. Drug companies constantly negotiate medication prices with payers such as Medicare, Medicaid, insurers such as United Health Care, Wellpoint or the Kaiser Foundation, and pharmacy benefit plans such as Express Scripts or CVS Caremark. To help lower the costs for patients, drug companies provide rebates – essentially refunds – to these payers. Since drug rebates can be 30-50%+ of the wholesale price and 88% of Americans are now on health plans, this rebate factor significantly impacts the “true” price most individuals pay for insulin. Unfortunately, health plan rebate information is not readily available, and although drug companies have noted that rebate rates have gone up, they have not provided the specific amount. That’s pretty understandable as this is competitive information – we’re merely pointing out that looking at retail prices is not the only relevant metric.

What may be causing this trend?

There are a few potential explanations for this trend, including the following:

-

Higher Rebates: First, payers are pushing harder for higher rebates. For example, both CVS Caremark and Express Scripts recently put pressure on Sanofi, Eli Lilly, and Novo Nordisk by excluding certain insulin brands from their coverage list. This forced these drug companies to offer larger rebates to these payers to stay on the their list, and in turn they may raise their wholesale prices.

-

“Biosimilar” Insulins: Additionally, the insulin market is set to become more competitive as “generic” (i.e., “biosimilar”) insulins loom on the horizon. A “biosimilar” insulin is made from the same protein structure as existing brands and at least theoretically has a similar glucose-lowering effect. Patents for Lantus expire this year in the US, while patents on Humalog (Eli Lilly’s fast-acting insulin lispro) and Novolog (Novo Nordisk’s fast-acting insulin aspart) also expire soon. These patent expirations open the door for others to introduce “biosimilar” insulin products that would likely be priced at a discount to the existing brands. However, it also means that current insulin brands may be increasing their prices now in anticipation of a more competitive market with “biosimilars” in the future. Biosimilars are not proven at present; insulin manufacturing is complicated and from what we have learned from market research company dQ&A, many patients are broadly positive about biosimilar insulins, although the devil is in the detail, with many concerns about potential differences in efficacy, among others. That remains to be seen.

-

Profitability: A reality is that drug companies need to sustain profits in order to run their businesses, including pay their teams, invest funds into research and development, build and market their products, satisfy their investors, etc. On the plus side, successful insulin companies can help lead to increased innovation – if companies felt they couldn’t continue to make profits in diabetes, we wouldn’t see any development on new therapies such as ultra-rapid-acting insulin. Ultimately, though, it’s devastating that high insulin prices could inhibit people from purchasing insulin. For some patients, particularly those with very stable blood glucose, older forms of insulin that are inexpensive (like NPH) may work fine. It could prompt multiple emergency room visits for others. Overall, insulin is a life-saving drug, and one that is necessary to prevent dangerous complications (which, in turn, lead to increasingly higher healthcare costs) – making sure patients have the right insulin is a big public health need and it is devastating when people do not have the right resources. Encouraging innovation from drug manufacturers and ensuring greater patient access to insulin are both key, as is making sure patients and doctors are well-trained on insulin use and are eager to use it. Right now, profits are down, patients have better access to insulin in the US overall (due to the ACA) though not the best ones, and many patients and doctors have considerable problems with training, largely because doctors (and nurses) aren’t well enough reimbursed on the training front.

The impact on people with diabetes and resources to help

Insulin pricing for those with insurance

For individuals with diabetes on health plans that require copayments for insulin, the out-of-pocket impact of this trend is modest. Copayment rates are going up – by how much exactly depends on the healthcare plan, but as Dr. Irl Hirsch (University of Washington) presented at ADA this year, these rises in copay costs are making diabetes therapies unaffordable for many people with insurance. Additionally, some patients might be forced to change their care regimen if payers continue to exclude certain insulin brands in an attempt to drive higher rebates. While a prescribing doctor can often override these restrictions, some might find it difficult to switch insulin brands, and the adjustment period could affect proper diabetes management. Bottom line, while many patients on health plans with copayments may not feel a major financial impact from rising price of insulin (depending on their coverage plan), some will find the increased burden of high co-pays challenging. To boot, their quality of care could be compromised if their insurance forces them to “downgrade” their insulin – from, for example, a branded insulin to, for example, NPH (for some patients this change might be fine – for others needing very stable insulins, it wouldn’t be).

Insulin pricing for those with low or no insurance

Individuals most impacted by the rising cost of insulin are the uninsured and the under-insured. These patients are forced to pay the ever-increasing retail sale price (which is increasing due to a variety of factors, including increased wholesale price) or a percentage of this price when buying insulin. The impact can be especially acute for patients requiring large quantities of insulin to manage their diabetes. As mentioned above, there is a chance that more affordable options become available in the future with the introduction of biosimilars – such a theory presumes, however, that biosimilars will work in exactly the same way as branded insulin analogs, and the diabetes community doesn’t have that level of information or confidence at present. As such, right now, a patient may have to make a trade-off between blood glucose control and affordability, since older human insulins (such as NPH) are always cheaper but can also lead to more hypoglycemia and weight gain and other issues stemming from their relative lack of stability compared to newer insulins.

Financial resources for patients

Fortunately, there are actions some patients may be able to take to reduce the burden from the rising cost of insulin. We recently discussed eight tips from endocrinologist Dr. Irl Hirsch (a fellow type 1 and diaTribe Advisory Board member) for optimizing diabetes management on a budget. Dr. Hirsch has been a great advocate over the last decade, in particular for patients who are at the lower end of the socioeconomic spectrum who cannot afford expensive drugs or in many cases expensive insurance and who have access only to government programs that allow only generic (or older) drugs. We are glad that many drug companies have programs in place to make insulin more accessible and hope to see more thriving commercial markets develop for newer drugs and devices so that even more programs can be created that serve a broader group. Below we have provided links and some basic information for several programs – for additional information on financial assistance programs for diabetes products, please see The Perfect D Blog’s financial resource page.

-

Eli Lilly offers free Humalog, Humalin, and Humalog Mix to qualified patients under the Lilly Cares program (call at 1-800-545-6962). To qualify you must be a US resident, you must not have paid prescription coverage, and you must meet household income requirements. A 120-day supply will be shipped to your health care provider's office for you to pick up and refills will be available during a one-year enrollment period.

-

Novo Nordisk offers free Levemir, Novolog, Novolog Mix 70/30, and Novolin to qualified patients under the Novo Nordisk Patient Assistance Program (PAP) (call at 1-866-310-7549). To qualify you must be a US resident, you must have a household income <200% of federal poverty, and meet other requirements. A 120-day supply will be shipped to your health care provider's office for you to pick up and Novo Nordisk will contact your health care provider 90 days later to approve a refill.

-

Sanofi offers several programs that entitle qualified individuals to free or discounted prescriptions including Apidra’s No Co-Pay Savings Program, the Lantus Savings Card, and the Toujeo Savings Card. To qualify you must be a US resident, you must not be on a government-funded benefit program, and all commercially insured patients are eligible.

The issue of prices and accessibility is a delicate one – it’s easy in information vacuums for patients to misperceive manufacturers as working under no constraints. The environment is more complicated than this, to be sure, as well as more dynamic. We certainly hope to see more patients getting access to better medicines, to see more patients who can do well on older medicines to take those medicines, and to see more companies doing well commercially making people healthier – that is what will further drive innovation in the ecosystem, and innovation that is accessible.